When I was in graduate school for my MBA, I took an entire elective class on bonds. While my transcript tells me that I got an A in the class, I think I promptly erased all memory of the content or knowledge from my mind the moment I left it, only to recover said memories a year or so later when going about studying for my securities licenses. You see, bonds are forever the less interesting side of the investment world. In the film, The Big Short, the opening monologue describes them like this: “…And if banking was boring, then the bond department at a bank was downright comatose.” I can attest that this is true.

Yet, bonds present an interesting investment asset for most people because, strangely, while their actual mechanisms are far more esoteric than common stocks and the equity marketplace, their general description makes a lot more sense to most people. “Lend money to a [government agency/company] and get paid interest.” As straightforward as anything seems! Yet, the pursuit of total return in fixed income investing introduces a number of complexities that most people might smile and nod at, but may not actually have a strong grasp of. So today, we’re discussing fixed income investing, and in particular, shedding some light on three particular nuances that can surprise the unwary fixed income investor.

Credit Risk & The Coupon Rate

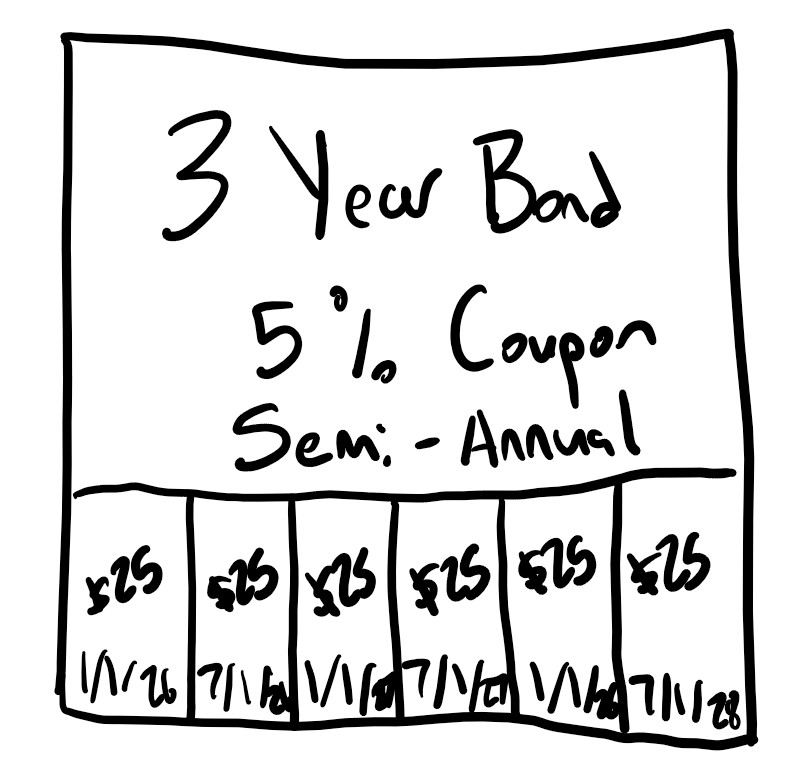

Because bonds are a fixed-income instrument, and as we just described, they’re essentially just lending money to a larger institutional borrower of some sort or another, they are fundamentally understood by their interest rate. The interest rate a bond offers to its lenders is described as a “coupon,” which used to be a literal slip of paper on the bottom of the bond that was cut off and sent to the issuer as the coupon came due, for which, in return, a borrower would send the coupon payment, or interest payment. My crude rendition of this is drawn below:

In the modern era, all of this is effectively automated by digital delivery of coupons and the related interest payments, but you have to remember that these bonds date back to the 17th century, in a time before such tools. In the present, however, the general mathematics of bonds remain the same, and so too does the mechanism by which the coupon rate is established. Effectively, the interest rate issued on a bond is a reflection of the credit risk it presents to its lender and the term for which the loan will be outstanding. The worse the credit of the borrower, the higher the interest; the better their credit, the lower the interest. The longer the term of the loan, the higher the interest; the shorter the term of the loan, the lower the interest. The relationships between credit and duration are not necessarily linear, but there is a basic logic to it. The riskier the loan and the longer the loan, the more interest the borrower needs to pay to make it worth the risk that the lender won’t get paid back.

Coupon rates can also be impacted by other factors. For example, bonds issued by government agencies such as school districts and cities are given special tax privileges compared to commercial bond offerings from private companies, and US Treasury bonds (notes, bills, and bonds, to be technical) are exempt from state and local taxes but not federal income tax. This dynamic means that agency, municipal, and treasury bonds invested in a non-retirement account can enjoy a greater after-tax yield than their corporate counterparts for equivalent duration and credit risk profiles, but that corporate bonds can be more favorable in retirement accounts because there is no material tax advantage to offset the potential for lower equivalent coupon yields. That said, you might still choose to invest in a treasury bond in a retirement account if the state income tax elimination benefit is nominal or you otherwise are seeking the general lower risk nature of lending to the federal government rather than a smaller issuer.

Par Value, Interest Rate Risk, and the Fed

When a bond is issued, it is typically sold in $1,000 denominations, which are then referred to as par value. When a bond is subsequently sold for more than $1,000, it’s described as trading at a premium, and if it’s sold for less than $1,000, it’s described as trading at a discount. The primary influencing factors for whether the bond will trade for more or less than $1,000 after its initial offering are the creditworthiness of the underlying borrower and the risk-free rate, typically measured by the shortest-term treasuries offered by the Federal Government. So, for example, if the 3-month treasury is being offered with a 1% interest rate to lenders (effectively 0.25% on the 3-month duration), then the subsequent interest rate any other borrower must offer to pay in interest is a reflection of the greater degree of risk such a lending incurs.

For example, today, a 30-year US treasury can be found offering an interest rate of 4.886%, while a AAA-rated corporate bond of the same duration can be found offering a 5.617% interest rate, and an A-rated corporate bond can be found offering a 6.558% interest rate. All of these interest rates reflect the extended duration of the loan as well as the underlying creditworthiness of the borrowers. Take on more risk, take on longer risk, and get paid more, so long as the borrower stays in business and solvent enough to pay back the interest!

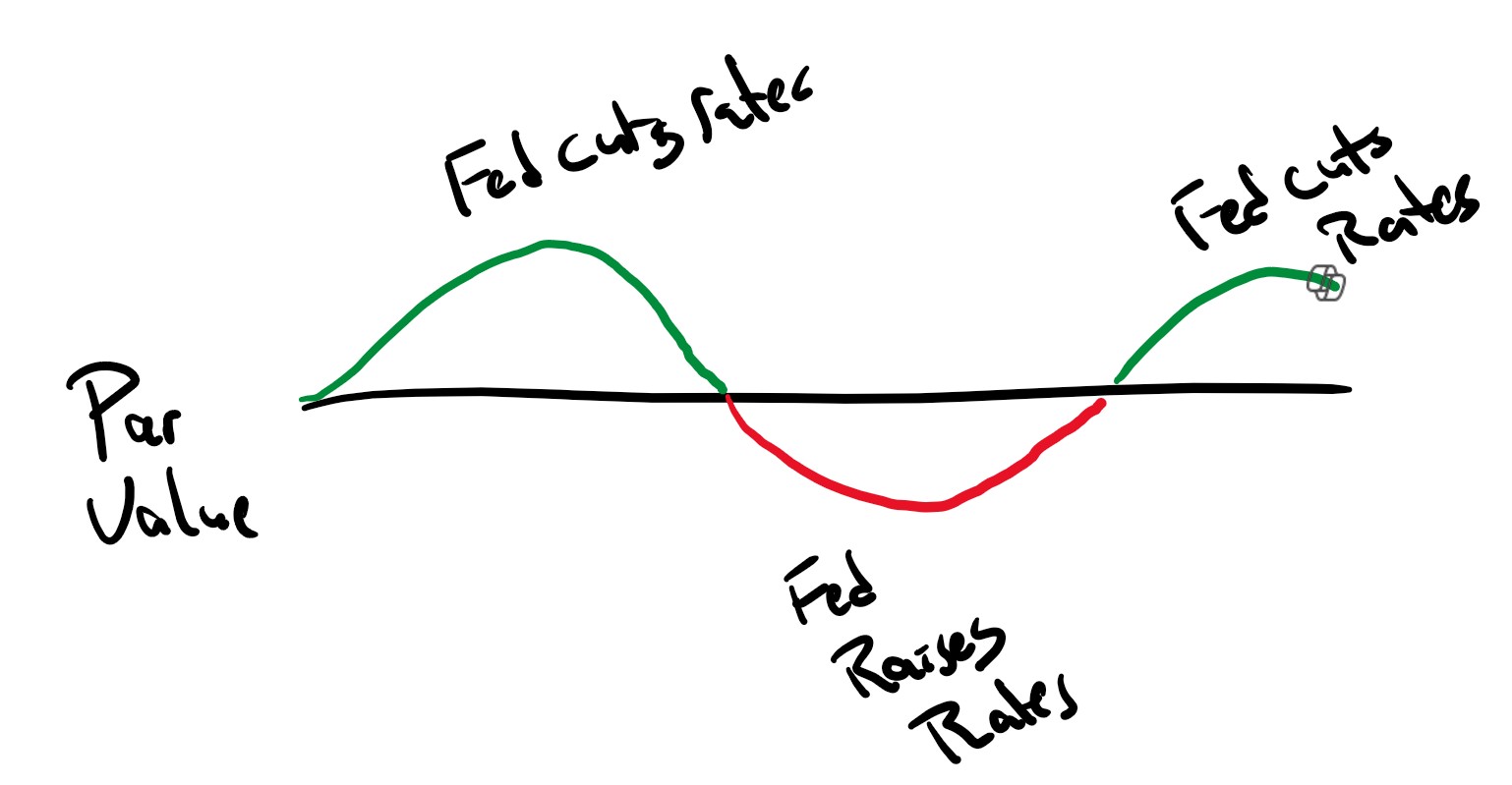

However, there’s a fair question that arises then: What happens when the risk-free rate, measured by the 3-month treasury, goes up or goes down? This typically occurs when the Federal Reserve increases or decreases its reserve rate, which is the rate offered to banks if they go to the Federal Reserve to borrow money to then turn around and lend or offer to their customers. When the reserve rate goes up, the 3-month treasury interest rate serving as a proxy for the risk-free rate goes up, and when the reserve rate goes down, the 3-month treasury interest rate serving as a proxy for the risk-free rate goes down. Consequently, there is an inverse change in the par value of bonds when the interest rate goes up or down. As you see in the diagram below, when the rates are cut by the Fed, the value of existing bonds tends to go up, and when rates are raised by the Fed, the value of existing bonds tends to go down. New or not-yet-issued bonds are not necessarily affected, because when they are issued to the public, they will reflect the then-current interest rate environment. Only after their issue with their face value increase or decrease with changes to the Fed’s reserve rate.

Maturity and Duration

The value of a bond in the secondary market after its initial issue is not as simple as the duration stated on the bond and the coupon rate offered. Because the bond might sell at a premium (above par value) or a discount (below par value), the underlying interest rate might be inversely decreased or increased. This is not the same thing as the coupon offered by the bond itself changing, but simply the value of the interest rate relative to the price the bond was purchased for. Because coupon rates are based on original par value, where an original sale of $1,000 and a coupon of 5% means the bond will pay $50 per year, the actual yield of the bond is enhanced when the bond is bought at a discount and is reduced when the bond is purchased at a premium.

For example, if a bond sold for $1,000 on its original issue with a 5% coupon rate is then resold for $950 because the underlying interest rates have changed or the creditworthiness of the borrower has gone down, then the yield would increase. For example, if there were 5 years left on the bond, it’s “Yield to Maturity” would increase to 6.19% annually, simply because the cost to buy the bond at $950 is less than the original par value of $1,000, increasing the rate of return on the bond, which will not only continue to pay $50 a year to the holder of the bond, but will also return $1,000 and not $950 to the holder of the bond when it reaches maturity. The inverse is also true. If the bond was trading at a premium of $1,050 and then came due in 5 years, the yield would be 3.88% because the borrower paid $50 more for the bond than it will pay back to them when it reaches maturity.

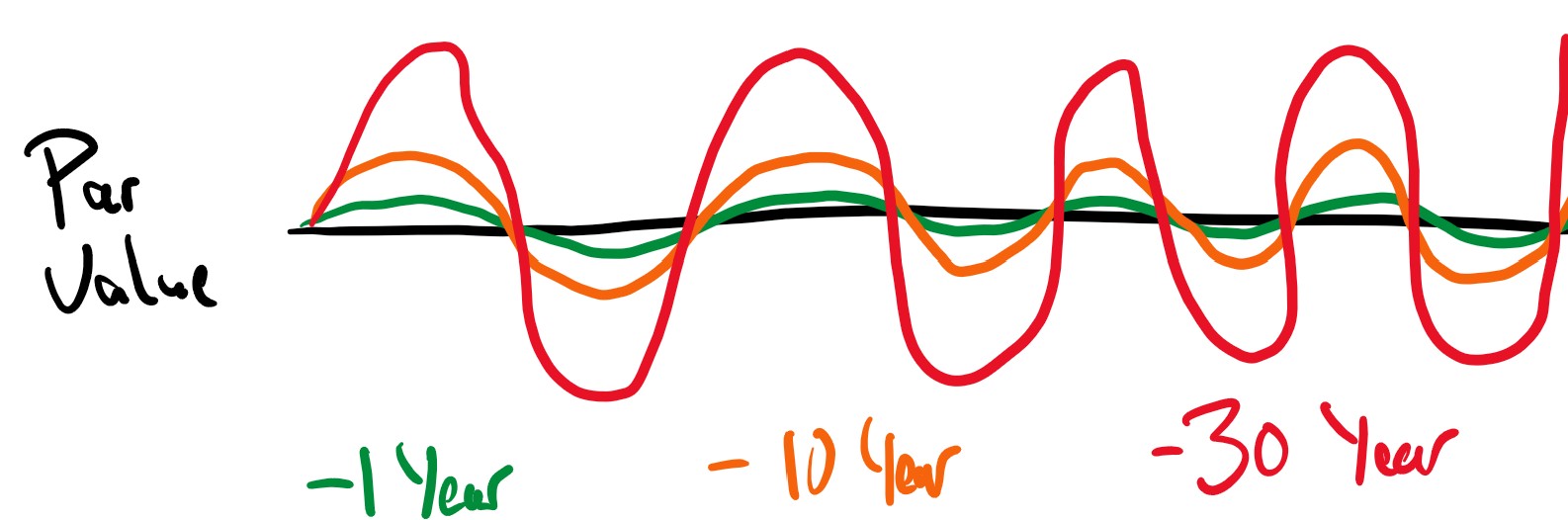

This then means that time is an important factor in bond yields, but also in how sensitive a bond is to interest rate change. The closer a bond is to its maturity, the less changes in interest rate matter because the borrower will soon pay $1,000 back to the lender. But the further away that time is, the greater the risk posed by the resale value of the bond in the marketplace. Thus, long-term bonds are generally more sensitive to interest rate changes than short-term bonds. For example, we see below how much the price of a bond might change, given the example of a 1-year bond, 10-year bond, and 30-year bond, given the same sequence of changes in the risk-free rate.

Is Allocating to Bonds Worth It?

A lot of the risk in bonds is relatively nominal compared to the volatility one sees in the stock market. While bonds themselves are not free from risk, as described by factors such as borrower insolvency and bankruptcy, interest rate risk, and even things like inflation, which can sap the value of the interest payments over time, they are generally treated as lower-risk assets because they are higher up in the cash flow hierarchy of who gets paid by a company.

The financial services author Nick Murray likes to make the argument that investors should be 100% equity invested and should forgo investing in bonds because he argues that you’ll always make more money in the long term by being the owner of a company rather than its creditor. In the aggregate long-term view, he’s generally correct, but bonds can serve a powerful function in hedging volatility risk and immunizing a portfolio with a specific duration and financial goal in mind. It’s meaningful as well that many risks faced by bonds with respect to their value in the secondary market can essentially shrink to zero as the bond comes due, leaving only the underlying risk that the borrower cannot make the payment of principal back to the lender.

We recommend bonds for our clients all the time because they serve as a more conservative asset class, and in some cases, they can present a high yield equivalent to the average yield of some equities at times. More importantly, while not universal, they are often only nominally correlated with the stock market, which makes them a useful tool for rebalancing when the equity side of the investment portfolio takes a hit from the latest economic or market crisis. All of which is to say, bonds are an appropriate tool for an investor who understands how they interact with external factors, and can be a powerful tool for those with extreme patience to let them mature. There is no risk-free lunch with bonds, but they’re an appropriate bet for many.

Dr. Daniel M. Yerger is the President of MY Wealth Planners®, a fee-only financial planning firm serving Longmont, CO’s accomplished professionals.

Comments 2

I worked for a former bond trader for several years, and got to hear all the “exciting” things about bonds, most of the time I was nodding off.. This is a good explanation, and since most people acquire bonds through ETFs or Mutual Funds, you should follow this up with the pros and cons of individual bonds vs bond ETFs.

Author

I’ve been told with great regularity that the best thing to write about is what people tell you they want to know more about! I suspect you already know all the pros and cons much as you did the underlying of today’s article, but I’ll gladly write it. 🙂