In the 1952 paper “Portfolio Selection” by Harry Markowitz, a paper that has since been cited 70,870 times in financial academic literature, the concept of “Modern Portfolio Theory” was born. The basic idea, which has guided our understanding of portfolios for the past seventy-plus years, is that portfolios should be constructed based on the average returns and variance of portfolios’ underlying asset classes (e.g. the average return and degree of volatility of large cap assets, small cap assets, international assets, and so on), and use those to mathematically optimize for reducing volatility and variance in return for optimizing for return. Essentially, to reduce the level of risk taken for the amount of reward pursued.

This theory has dominated the idea of asset allocation since its inception, with terms like “The Efficient Frontier” becoming ubiquitous in the construction of portfolios. This is important, then, because our discussion is going to take modern portfolio theory and its product for granted, and instead highlight a problem that it renders all but moot: The idea of comparing results. Specifically, the idea of “splitting the baby” when it comes to your investments: Trying one investment strategy over here and a different one over there, or hiring a portfolio manager to handle one half of your portfolio while you or another portfolio manager handles the other.

We’ll discuss why such strategies are generally scientifically invalid in the first place, but also what factors do have more impact on the overall outcome from an evidence-based perspective.

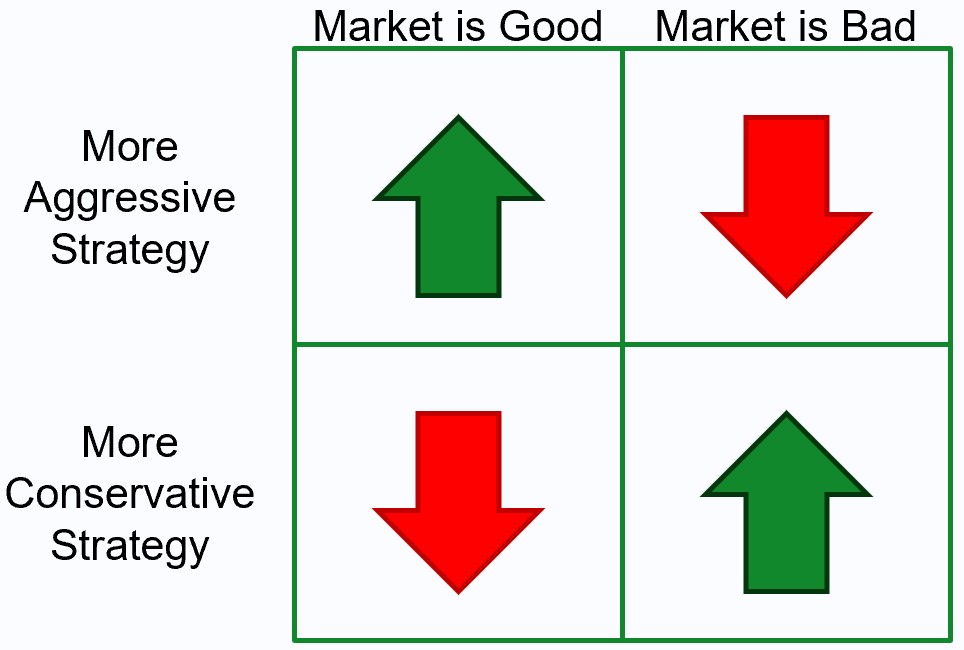

The Four-Box Matrix

Taking the assumptions of modern portfolio theory into account, the outcome of comparing two investment strategies (whether that be funds, managers, tactics, or timing) is all but guaranteed to produce a specific set of predictable results, as described by our four-box below:

When you decide to split up your portfolio across two strategies, one is inevitably more aggressive, and one is inevitably more conservative. This might not be apparent if you hire two portfolio managers charging equal fees, and each constructs a 60% equity and 40% fixed income portfolio, but it could be more obvious as you get into the sub-asset classes such as small cap growth vs. small cap value, broad international vs. emerging markets, and so on. And the results are likely to be even more pronounced if one constructs a 100% equity portfolio while the other constructs a 60-40 portfolio as just described. If the markets are positive and growing, the 100% equity portfolio manager will probably crush the 60-40 portfolio manager, and if the markets are declining, the 60-40 manager will look like a genius for having hedged against the downturn risk, while the 100% equity manager will look rather foolish and overly aggressive.

But neither thing is true. There is no evidence that any portfolio manager of any tenure or skill can reliably predict the course of the economy or the market. Examples such as Bill Miller, who ran the top value fund for 14 years straight and then took the 98th lowest percentile of performance in years 15 and 16 and the 99th lowest percentile in year 17. Or Ray Dalio, who built the largest hedge fund in the world, has predicted the market would crash dozens of times over the past few decades but has only been right on a rare few occasions.*

*This is a commonly observed phenomenon in the marketplace. Portfolio managers will regularly make substantial and dire predictions about the market over and over again so that when they are finally correct by sheer volume of guesses, they can point to a time they got it right and say “look, I saw it coming and no one else did!” A far better measure of their genuine beliefs is how they’ve managed money during such predictions. To no one’s surprise, such bearish predictions are seldom accompanied by going to cash ahead of the crash or otherwise shorting the market to make money on its decline.

So we, the average investor, are left with a basic premise: assuming reasonably competent investment selection, all we can do is target higher returns while assuming greater volatility (risk) as the price of such bets, or target lower returns and forgo the long-term upside potential for the sake of a smoother ride; and comparing the performance of one strategy against another is seldom a test of skill or competence, but mere luck of timing. Be aggressive when the markets are good to you, and you’ll win; be conservative at the same time, and you’ll lag. Be conservative when the markets are bad, and you’ll be glad you didn’t take on too much risk; be aggressive when the markets are bad, and you’ll be smarting for it. The only equalizer beyond that is a longer time horizon with patience and discipline to stay invested.

The Siren Song of Alpha

Despite the obvious evidence of the four-box matrix, investors are easily misled by the promises of more and better. Certainly, you can understand the appeal of a good story: Buy this indexed insurance policy and you’ll never see a risk of loss1, Crypto has been the best performing asset of the past decade2, wait on cash until the market goes down and then buy in, and so on. Whether these are pitches from insurance agents, brokers, or financial influencers, the promise is the same: listen to me and you’ll be wealthier than if you hadn’t. It could even be true, to be fair!

But the real underlying problem is that no individual portfolio manager or investment manager makes decisions beyond asset allocation and product selection that will materially improve the outcome, and in turn, all other offerings are based on a fundamentally misguided belief that they are somehow exceptions to the rule; the rule being that any “alpha” they might produce is often coincidental and temporary, not the result of superior knowledge or strategy.

For example, as money managers, we could wait until an opportune quarter or year comes across our portfolio’s results and then rush to market to brag that “portfolio A has beaten its benchmark by 2% in 20XX!” Doing so might draw attention, and even clients or investors. But what’s the point of advertising performance when you don’t fundamentally believe, nor is there any evidence for, the idea that we will outperform the markets by any consistent or material metric long term? As some say in the sales world, “win by price, lose by price,” but the same can be said of investments: “win by performance, lose by performance.” We’d rather be thought of as valuable for more than just the money we can make for clients, because as the evidence shows, any reasonably competent portfolio manager can do that one thing.

Rather, we view our “alpha” with our clients not in the form of investment returns or overall wealth growth, but primarily through client retention. We’ve enjoyed long-term relationships extending over a decade with dozens of households, and had the pleasure of working with over 98% of our clients year over year. Whether that’s because we’re excellent investors, or great financial planners, or just really fun to spend time with, we can’t really say. We can only measure our success by how long our clients work with us, thus feeling like the relationship and our services are valuable, and how consistently most clients keep that feeling long term. We could even say it’s a consolation that most of our client attrition is due to clients passing away over the long term, but that isn’t quite the warm fuzzy we wish it was.

The Things That Will Skew the Four-Box

If we take luck out of it and just look at things objectively, then we’re left with the other things that can tip the scale one way or another. These are things within your control or the control of your portfolio manager, but ultimately will impact the outcome beyond the basic asset allocation.

First, cost. It is to no one’s surprise that if you compare X minus low cost and X minus high cost, that X minus low cost will win the day. This is important when it comes to commodified choices, such as which S&P 500 Index Fund you want to purchase; some are available for 0.03%, some are available for 0.19%. It’s fairly plain that the result of the one costing 0.03% is probably going to outperform the one costing more than six times as much, but that doesn’t make cost everything. While I don’t think the adage “buy cheap, buy twice” entirely applies to investment products, the inverse can certainly be true.

There’s a recent batch of investment products called “long short” strategies, which we’ve briefly touched on before, but that fundamentally attempt to combine an active management portfolio strategy with leverage and options to create a portfolio that somehow generates excess returns above the results of the market both through a combination of intelligent portfolio management but also incurring regular tax losses to wipe out the gains, such that you’re somehow making more money net of tax than you would if you’d picked the passive portfolio option. All of that could be true and possible in some respect, but one factor that’s immutable is cost. Such strategies regularly charge product fees of 1.1%-2.5%, and in the hedge fund world, such strategies can even cost the traditional 2-and-20 (2% management fee plus 20% of profits above a hurdle). I don’t know that a product charging 1.1% or 2.5% can’t be more than worth the cost (only time and year-by-year performance can tell), but if I simply look at the underlying assets and the long-term performance of said underlying assets, then I suspect the long term result will be no better than X minus cost, and therein we wonder whether such above-market costs are warranted.

Such things also tip us into the next category of “things likely to tip the scales,” which is the very idea of active management. While the since-inception argument of active management has always been to pick winners, avoid losers, and protect the downside, the inevitable arc of history shows quite thoroughly that such things are generally impossible the longer time goes. In a time period as short as a year, you might have about a 1 in 4 chance of picking a sharp large cap portfolio equity manager who can beat the market. But keep flipping that coin twice a year to see how long it keeps landing on “heads” over and over, and I think you’ll find it comes ass-end up sooner than later. And of course, active management is often less tax sensitive because of the frequency of trading that active portfolio analysis often requires, which then increases the tax drag of such investment philosophies.

Time is the Great Equalizer

In portfolio management, there’s an almost gravity-esque observation akin to a law of physics: reversion to the mean. That which outperforms must inevitably underperform, and that which underperforms must inevitably outperform. While I think this is somewhat magical thinking (at least that those that underperform must someday outperform), it is a general observation that anything that is too good eventually ceases to be as the market swings towards it and smothers whatever advantage there may once have been. The cute local bar eventually becomes too popular for its own good and what was once great ceases to be. Such is the way of things.

All of this to come back to the core premise: there is no comparison exercise that is likely to yield a scientifically valid long-term result. Split your portfolio between a long-short product and a skew of index funds, and you’ll make more money on one than the other for now. Go all-in on crypto and you might get rich now and broke later. Buy a complex insurance product with guarantees to hedge the downside and then be grumpy for a decade before the next big downturn hits and all the hedging finally “pays off.”

Whichever one wins in the short term is likely to matter less than which one outperforms long term, but because you can’t see the long-term result, you’re more likely to be swayed to overweight favor to whichever strategy outperformed in the short term. Such temptations inevitably lead to return chasing, that most classic of investor follies. “I must buy this thing now that it’s more expensive” has never made any more sense now than it ever did then.

Therein is the point: assuming you or your portfolio manager are competent, set long-term goals, and build a portfolio that is statistically the most likely to accomplish the long-term goals. From there, let it run, monitor accordingly, and focus your time and energy on more important things, like winning your World Cup bracket or finally cleaning out the garage.

Dr. Daniel M. Yerger is the President of MY Wealth Planners®, a fee-only financial planning firm serving Longmont, CO’s accomplished professionals.

Comments 2

Is “winning your World Cup bracket” gambling? Betting? Dan! How does that fit into the persona of a dependable financial planner? Admitedly, that is more fun than cleaning out your garage.

Yes, steady wins the day.

P

Author

Confession time, Phyllis: I barely know anything about sports, haha.