Last week, we provided a layman’s overview of bonds, and if you haven’t read it yet, you can find it here. At the urging of one of our very well-informed clients on the subject of bonds, this week we’re moving on to the natural extension of bonds by which most everyday investors buy them, which is through bond funds. While there are substantial differences between index bond funds and active bond funds, we’ll share a little bit of history on the bond fund “product” and how it has evolved over the years, and then get into the nitty gritty of what matters to you as an investor when deciding whether to invest in a specific bond offering versus a bond fund, whether that be an index bond fund or through an active bond manager.

A Brief History of Bond Funds

Not unlike what was said about the bond department in banks, bond funds have historically been just as boring as bonds themselves. This was because, like banks, most bond funds were run by financial institutions trying to offer money market products or otherwise trying to offer FDIC-insured products like certificates of deposit (CDs). Another major consumer of bonds was insurance companies, which ran multi-billion dollar portfolios of bonds, largely to guarantee the general accounts of mutual insurance companies or the investment portfolios that reinvested the premiums paid in by various policyholders. It wasn’t until the 70s and 80s that the concept of “total return” bond investing came into vogue, where rather than buying bonds solely to be held until maturity, bond managers instead sought pricing and duration inefficiencies caused by changes in credit rating and the underlying risk-free rate environment to generate greater yields based on the yield to maturity rather than the coupon rates.

This has essentially left us with five mega-categories of bond fund strategy, for which there are then many subsets and variations. Whether index or active, these are:

- A total return approach where bonds are bought and sold by an active manager for the purpose of obtaining returns greater than the coupon yields on the bonds themselves.

- A maturity-focused strategy where a fund buys and holds bonds with a specific maturity date, e.g., “every bond in this fund matures in 2035.”

- A duration-focused strategy where the fund aims to hold and then divest of bonds over time that do not match the general duration goals of the investment portfolio. These are typically bifurcated along categories such as ultra-short, short, intermediate, and long duration strategies, which are measured in years or decades.

- A credit-focused strategy where the bond fund deliberately invests in highly credit-rated or lowly credit-rated bonds in order to hedge credit risk or pursue higher returns while leaning into credit risk.

- Aggregate bond funds that simply do not have a preference for any particular factor of the bond, other than perhaps its tax treatment, e.g., aggregate treasury, aggregate corporate, aggregate municipal, or aggregate international bond funds.

A “sixth” category would simply be the introduction of international bonds into any of the aforementioned categories, but that gets us into the topics of international policy risk, exchange rate risk, and other factors beyond the scope of what we want to discuss today.

What “You” Are Looking For in a Bond Fund

Recognizing that you are a singular individual among many billions of other singular individuals, what you’re looking for in a bond versus a bond fund can vary enormously. Like most things in investing, the best answer is typically derived from the best solution to your specific problem or your specific objective.

For most investors with a non-specific goal beyond “retirement” or “investing extra cash,” the primary drivers of a bond fund investment are going to be diversification and cost structure. This will lead many to invest in an aggregate bond index fund with a low expense ratio and to call it a day; typically, a corporate bond fund, though someone seeking security might use a treasury fund, and someone else looking for additional net-of-tax return might look to a municipal bond fund for its tax advantages. Ultimately, this investor is de-risking what otherwise might be a largely equity-based portfolio.

However, for an investor with a more specific view of their timeline and objectives, for example, they know they plan to pay off a mortgage with a lump sum when their adjustable rate comes due, they might elect to buy individual bonds or a bond fund with a maturity that ties to the due date of that specific financial event. Doing this is called “immunizing” your bond portfolio, because you’ve taken out all the risk considerations pertaining to the secondary market, interest rates, etc. You’re simply buying a bond or a bond product that will mature on schedule and leave you with the money you expected when the bond matures to then fund your financial goal, or at the very least to complement the money you’re putting toward that goal.

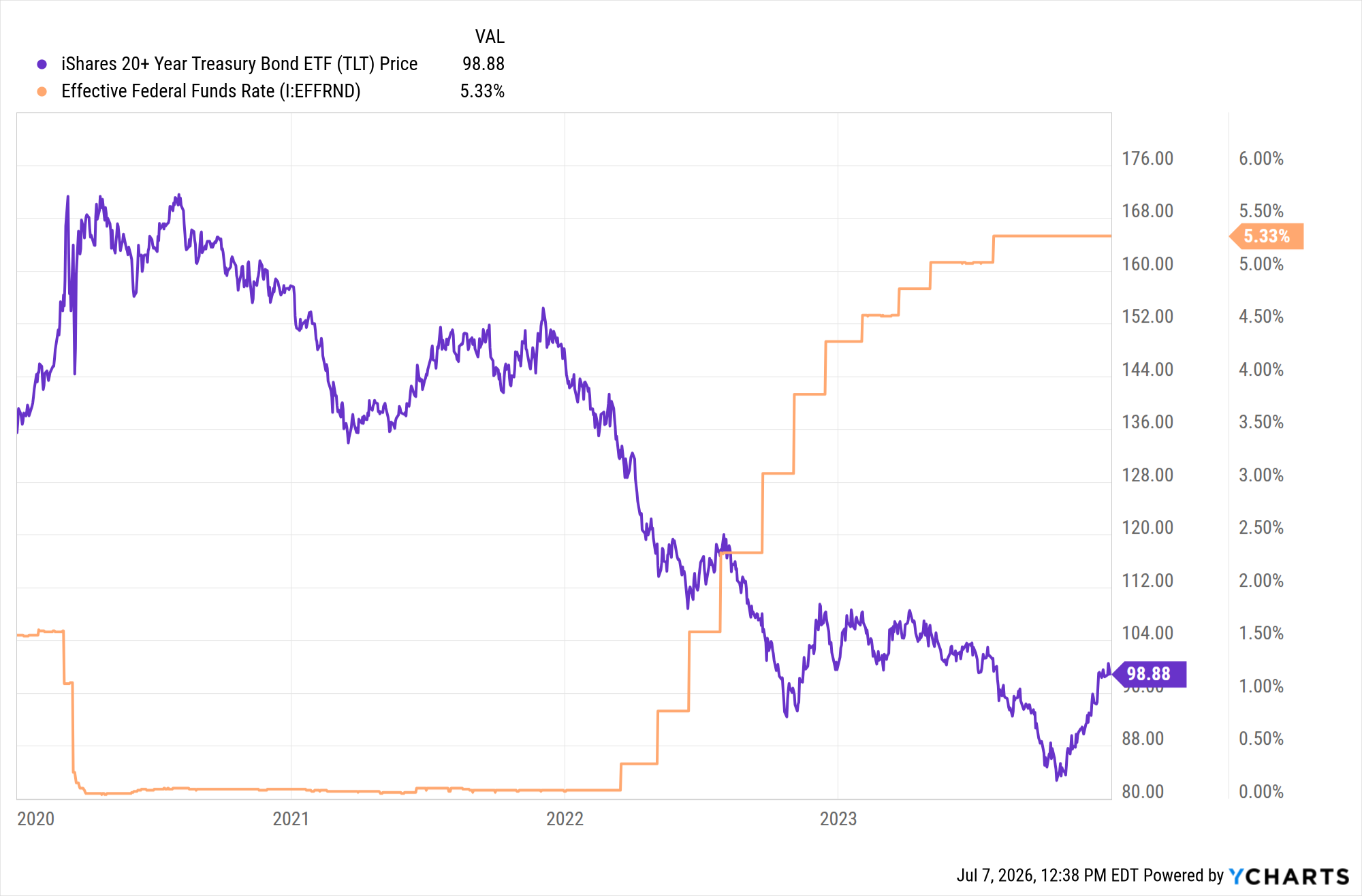

In turn, a more active bond investor, particularly those working with a financial planner or portfolio manager, might take a more duration-sensitive approach to a broader fixed income goal. For example, when interest rates are higher, and the yield curve is not inverted (meaning short-term bonds pay less, long-term bonds pay more, all things otherwise being equal), it’s likely that a fixed income portfolio manager might buy longer-term bonds for their higher yields. Yet, that same manager needs to be more conscious and aware of interest rate risk. If interest rates drop, then that long-term bond fund will do well in the short term, but if interest rates go up, then that bond fund will get crushed. For example, look at the performance of the TLT ETF, a fund that holds 20+ year maturity US Treasuries, which we held going into COVID and divested in early 2022 before interest rates began to rise after the Federal Reserve had tanked rates down to zero in response to COVID.

Chart shows Federal Funds Rate and share price of the TLT ETF from 01/01/2020-12/31/2023. This time period has been selected for its clear demonstration of the inverse relationship between Federal Reserve Rates and long-term bond values, but is not a recommendation to buy or sell TLT or any other specific security.

As you can see, the value of TLT shares shot up when the Federal Reserve tanked rates and then proceeded to taper down over the following two years until the Federal Reserve began to raise rates, at which time the underlying bond values tanked because what had brought them up in the first place had come back down to earth. A more active bond manager would reflect on the probability of the event that, after rates went to zero, at some point they would go up, and while being in long-term bonds before the drop was profitable, would have to recognize the potential risks of staying in them when rates came back up. None of that is to say that you should be an active bond manager or otherwise need to hire one, but just to note that while an aggregate bond index captures all the good and all the bad of the bond market as is the nature of such an index, there are some fairly obvious mechanisms at work in the bond market that materially can impact their value, and a prudent manager can do the work of trying to navigate between the lines of interest rates via duration adjustments.

Some Underlying Issues of Individual Bonds & Bond Funds

One thing many investors don’t realize is that bonds are not as marketable or liquid as stocks can be. We are used to buying Apple stock or S&P 500 index ETFs with the tap of our thumb on our phone via a trading app, so it can come as a surprise to some investors that buying individual bonds can take a bit more time. For heavily traded cash equivalents like 13-week US Treasuries, the market is essentially enormous enough that trades can happen almost instantaneously. But when you buy an individual bond offering from a specific municipality or corporation, you may find that there is no active market for that bond, where there’s constantly a group of people looking to buy it from you or sell it to you. Consequently, many individual bonds have to be put out to bid, whereby if you are buying you may find you have to pay as much as a few percent over the current market rate for the bond simply because you’re the only person looking to buy in a marketplace that had no sellers, or vice versa, you may have to sell at a discount of a few percent if you’re the only party looking to sell in a marketplace that had no buyers. Essentially, we can end up paying a transactional cost in the bid-ask spread between what the bond is worth and the “make me buy” or “make me sell” prices others are willing to pay.

While it can seem like you avoid this issue entirely by buying into a bond fund, that’s only partially correct. While you won’t have to go out to bid on a bond ETF like “AGG” or deal with trading spreads when you put in a redemption request from a bond fund like “PONPX”, you’re still eating the transaction bid-ask costs inside of the fund. While many bond funds charge a very nominal expense ratio, and even though they can benefit from enormous economies of scale in their bidding, ultimately, bond funds can still incur the same buying and selling costs as retail consumers of individual bonds because their underlying portfolio demands that bonds be added or subtracted in alignment with the investment thesis. This can be less of an issue in a specific-duration bond product that matures on a specific date, but if you invest in a long-term bond fund, that bond fund will have to divest of bonds that are closer to reaching maturity than the definition of long-term permits, and in turn, will have to use the proceeds to buy new long-term bonds. Sometimes that turnover is profitable, sometimes it’s not.

Our Take on Bonds vs. Funds

To put it simply, we believe the vast majority of investors we work with don’t have a duration-specific objective that’s assisted by buying individual bonds. It can make a lot more sense for municipal bond investors in a specific state with high income tax rates, like New York or California, to buy New York or California bonds, and it can make sense when you do, in fact, have a specific timeline that you want to immunize your interest rate risk for. But otherwise, what we see is that the vast majority of clients look to buy bonds not because they’re a great financial asset, but because they want a degree of less volatile “counter-weight” in their portfolio to offset rebalancing when the market is down or to provide a more stable “base asset” when the market is good.

There are arguments to be made that the transactional costs of individual bonds are too high for most retail investors to really make sense of buying them, and in turn, that there are too many fundamental issues in the bond marketplace for big index options to make a lot of sense for clients. For what it’s worth, we’ve always focused on approaching bond investing from a duration-lens because while we may agree or disagree with the economic assessments that guide the Federal Reserve Board’s monetary policy, there is a basic mathematical calculus that tells us what happens when we’re too long or too short in duration for a particular interest rate environment, whether that means we should increase or decrease our duration appropriately.

We’ve said before, and we’ll always say that while we do own a crystal ball (it’s on the bookshelf next to the entrance of the office), the darn thing doesn’t work. Fortunately, the Federal Reserve has historically not been particularly subtle about what it’s doing, but that remains to be seen under a new chair of the board who seems to be interested in taking more of a “do your own homework” approach to telegraphing what the Fed may or may not do in the future.

For now, you’re probably best off investing in bonds insofar as you want safer assets, but whether you want to take a more active or passive approach to your bond strategy is certainly a personal decision, and whether you feel better served with individual bonds or bond funds is just as unique.

Dr. Daniel M. Yerger is the President of MY Wealth Planners®, a fee-only financial planning firm serving Longmont, CO’s accomplished professionals.