Yesterday I had the rare privilege to have lunch with Dr. Brad Klontz. A financial psychologist, CFP® Professional, and influencer with about 1.4 million followers across platforms such as TikTok and YouTube, Dr. Klontz is well known both within the financial planning space and without. His particularly famous research contribution to the field of financial planning is the concept of money scripts, subconscious values and beliefs about money, and how those play into the decision-making and feelings we have around money.

Much of Dr. Klontz’s content in the social media space is focused on creating financial self-efficacy for young people and low-income households. TikTok clips and YouTube videos cover topics like keeping up with the Joneses, avoiding expensive status symbols, and spending addiction. In addition to this, he’s authored and co-authored a dozen books on financial psychology and personal finance for audiences ranging from academics to everyday people. His latest book, a copy of which he kindly gifted me yesterday during lunch (full disclosure), is “Start Thinking Rich: 21 Harsh Truths to Take You from Broke to Financial Freedom,” which he co-authored with Adrian Brambila, an influencer who creates content on side hustles and second incomes.

It’s perhaps noteworthy that the working title of the book was “Stop Being Poor,” but we’re not really here to talk about the book, but about the tone it strikes and what it says about financial experts. You might reasonably infer that there’s a bit of a no-nonsense attitude to Dr. Klontz when you look across his works, including other titles such as “Mind Over Money” and “The Financial Wisdom of Ebenezer Scrooge.” Contrary to the titles, Dr. Klontz is about as kind but as straight a shooter as they come, and that’s the point. Today, we’re talking about attitudes people often express on the topic of money, and what experts like Dr. Klontz have to say about them.

Intrinsic > Extrinsic

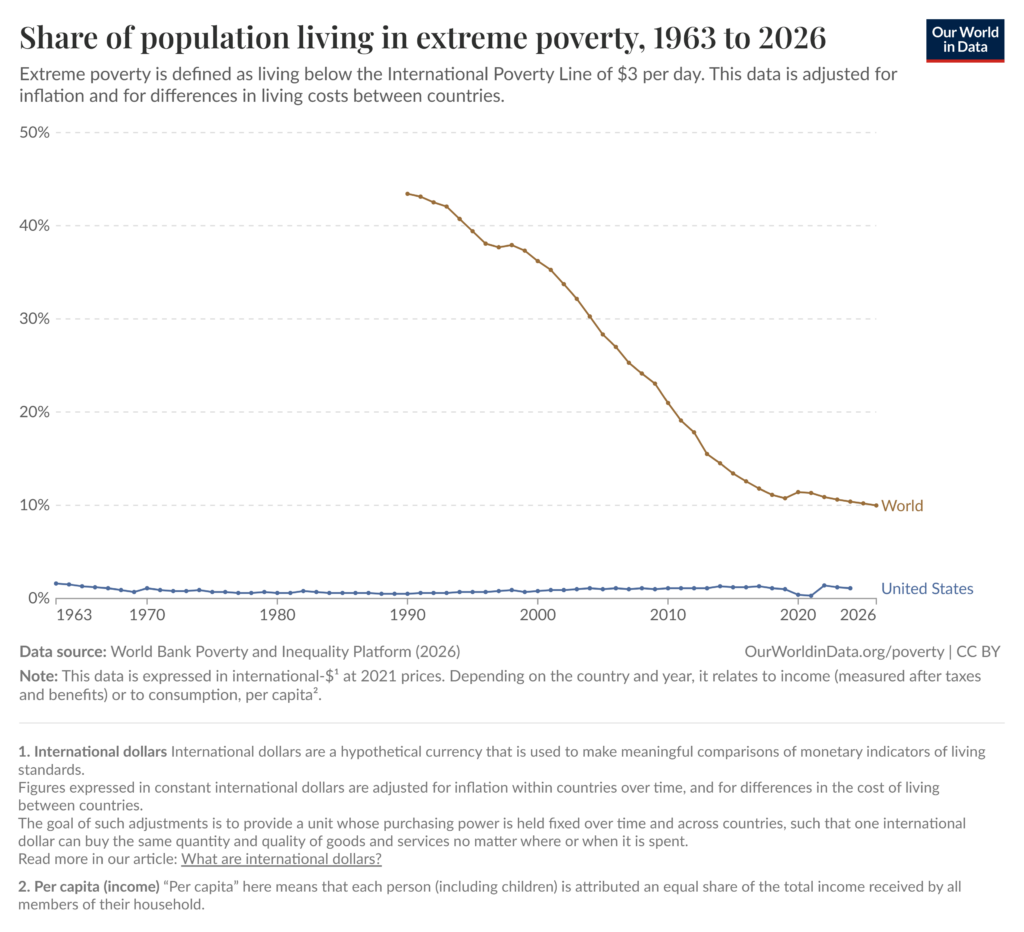

It is not uncommon for people talking about money to speak about it in externalizing and negative terms. “Billionaires shouldn’t exist,” “the rich need to pay their fair share,” “Capitalism doesn’t work,” “wealth inequality has never been greater.” All of these remarks place judgment on an imperfect world and put money at the heart of that imperfection. They draw attention to the extremes of the financial system, highlighting billionaires or pointing at the difference between the wealthiest and the poorest and ascribing an ill intent to the existence of that difference. There is nothing wrong with wanting the world to be a better place where everyone is better off. Permit me then to point to a contradictory observation: Despite capitalism having never been a more dominant economic system in the world, both domestic and global poverty are at all-time lows.

Source: Our World in Data

If the system supposedly at the root of all ills in the world is thriving at the same time that the finances of the world are improving year over year, what can be made of that? Simple: Capitalism and the world economies have thrived because of disintermediation. Centralized economies that dominated the 2nd world over the 20th century have largely lapsed into obscurity or collapsed entirely because centralization of economic responsibility was far less efficient than individual agency; in turn, those economies that have turned away from capitalist systems over the past century and leaned into more centralized management of economic issues have seen massive inflation in the value of their currencies, unemployment rates, and a general stagnation in the growth of their economies.

But those are all macroeconomic factors. What does decentralization vs. centralization say about personal finance? Simple: There is nothing more efficient or effective at improving your financial situation than your own action. While there is nothing wrong with decrying inequality or wishing for a better world, nothing is going to individually improve your situation more than you taking direct ownership of your circumstances and doing something about them.

That isn’t to say it’s easy or that the playing field for doing so is fair, but simply to acknowledge that nothing will more rapidly improve your situation than trying to personally improve your situation.

Ruinous Empathy

In the book “Radical Candor” by Kim Scott, she highlights a two-dimensional axis by which feedback should be given: Caring personally and challenging directly. Fail to care personally or challenge directly and you’re simply engaging in manipulative insincerity, challenge directly without caring and you’re engaging in obnoxious aggression. The ideal combination is to care personally and challenge directly, thus resulting in radical candor. But here we draw attention to the last specific example: caring personally without challenging directly, which Kim Scott defines as “ruinous empathy.”

In other words, by caring more about someone’s feelings or sense of self esteem more than you care about actually helping them, you simply concede to the difficulty of their conditions and fail to try to empower them to do something to improve them. This can be as passive as doing nothing to the detriment of people you otherwise care about; you can even do this to yourself.

Personal finance is ultimately a domain about self-efficacy because it is the concerted effort of both financial literacy and action that actually produces results. No amount of reading about investing will get you anywhere if you ever fail to put a dollar into something with the potential of appreciating in value. No number of budget tracking apps or personal finance books will make you master your cash flow unless you actually conduct your finances with a degree of discipline and consideration. No amount of not thinking about bad things happening will prevent bad things from happening, whether that be losing your job or getting into an accident.

It is common in the public discourse about personal finance to lay the blame of your situation at the feet of forces beyond your control. But as the Venn diagram shows: There are things that matter and there are things you can control, and your attention should be focused on where those things overlap. There is a reason that the Japanese concept of Ikigai doesn’t stop with “what you love” and “what you’re good at,” but also encompasses “what you can be paid for” and “what the world needs.”

Tough Love

None of this is to say that the world is perfect or that everyone needs to pick themselves up by the bootstraps. Plenty of problems are beyond our control and plenty of people are effectively trapped in circumstances beyond their control. But if you’re the type of person to have read this far into the blog or the type of person to be subscribed to a financial planning firm’s newsletter, you are probably not one of those people. It is meaningful to take responsibility for your money and your life. Whether that is going back to school, paying down debt, or controlling your lifestyle to live within your means, the options available are plethora. But no one’s circumstances are ever materially made better by focusing on the negatives, but putting energy into effectuating positive and controllable outcomes. Money is no different.

Dr. Daniel M. Yerger is the President of MY Wealth Planners®, a fee-only financial planning firm serving Longmont, CO’s accomplished professionals.

Comments 1

Well said Dan. I’ve seen this attitude of helplessness with personal finance too many times. Of course everybody’s circumstances vary, but taking agency is the first step.