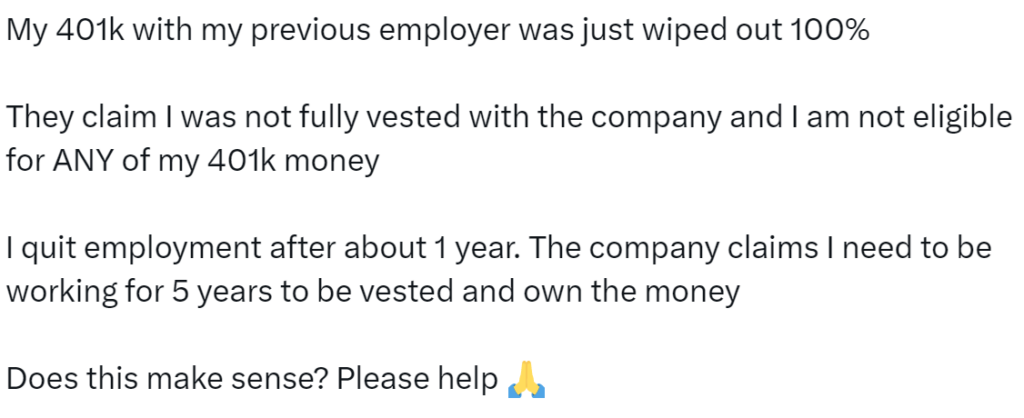

Yesterday, as often happens, a tweet went viral.

Now, notably, I’m not here to talk about vesting schedules. Vesting schedules would be contrary to the title, and might be the “least sexy” thing we could possibly discuss. Suffice it to say, vesting schedules exist because employers want to incentivize employees to stay longer than minimum terms with the company. Other employers don’t have vesting schedules because they’re generous or want competitive compensation packages. The end.

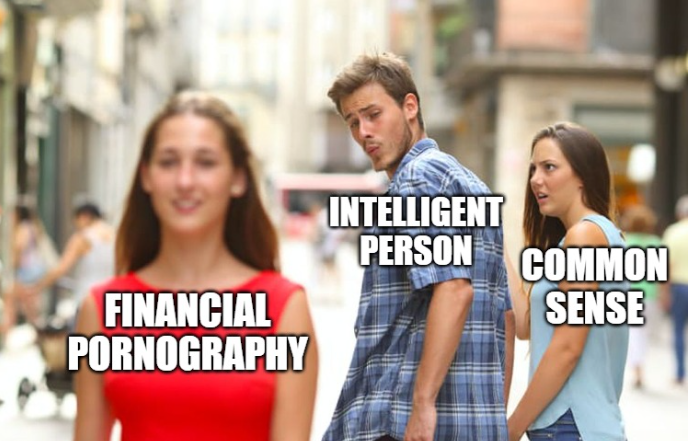

No, we’re here to talk about the “who” behind the post, or rather, the archetype of the “who” behind the post. I won’t name them (not that you couldn’t google and find this person easily), but they have an account with 14,000+ followers that started barely over two years ago on Twitter, touting the “benefits of dividend investing” and inviting people to “join them on the road to financial freedom.” The obvious irony here being that despite the quickly growing following and promise of leading people to financial freedom, the person behind this particular profile clearly knows nothing about America’s most popular retirement plan and its basic functions.

These types of influencer accounts are popular on Twitter. Pick a particular financial niche, whether it be index funds, dividend investing, factor investing, crypto, ESG, or any other ultra-specific type of asset, and post about it non-stop. Of course, this phenomenon isn’t limited to Twitter, with insurance salespeople on TikTok, real estate “moguls” on Instagram, and so on. So why bring it up? Because while some people behind these accounts are well intended people sharing their journey, others are grifters and con artists, and among the two there are countless people who simply do not know what they’re talking about. So today, we’re talking about why sex sells in the financial media space, and why you should be a bit more faithful to yourself.

Financial Pornography Networks

The original form of “sex sells” in finance was from a pre-regulation era. Laws were passed in the early 20th century to prevent people from selling “nothing more than blue sky,” as one judge at the time opined. Yet, over the many decades sense, thousands of newsletters, media channels, and popping heads have shown up to produce what is colloquially known as financial pornography. This content is often excitement driven: “Buy now, sell now, the market is about to implode, precious metals are the only thing that can protect you, don’t miss out on this opportunity, buy buy buy!” Yet, as anyone with a functioning memory can recall, this type of content is daily, apocryphal, and ultimately does more harm than good. One famous purveyor of such content is so famously wrong that a “reverse index” of their advice has beaten the S&P 500 index by 3.8% annually over the past five years (3/31/2017-3/31/2023). Yet why do we call it financial pornography? The debate over actual sex work and products aside, the basic idea is that financial pornography is excitement, enticement, and arousal without substance. No matter how much of it you consume, how excited, anxious, greedy, or fearful it gets you, it will never actually provide you with anything of material substance or value. It is, at its best, a genre of entertainment product. At its worst, it’s destructive of your life and finances. It doesn’t matter whether it’s someone on social media posting from their basement or broadcasting 24/7 on television from a tower in Manhattan: it has no actual value.

Why is most legitimate content so… bleh?

A client asked me recently if I write this blog. I was taken aback. “Yes, I write it. Every Tuesday morning, come rain or shine, I write the blog.” “Really? It’s just so professional, I sort of assumed you had someone writing it for you.” They told me. Back patting and strange compliments aside, it threw me off. One of the things that I’ve always enjoyed about writing the blog is the opportunity to share my voice and to speak on topics that any sort of canned content would never dare try. Case and point, find some canned financial media content out there talking about “financial pornography”!

Yet, if you’ve ever spent much time contemplating the advertising and marketing of financial firms, it might occur to you that much of their programming and advertising is boring. An elderly white couple walks hand in hand down a beach before settling in some Adirondack chairs, a young black couple look reassured as they sit down at a table in a nice office with a woman in a suit, a welder pulls off his goggles and smiles confidently into the distance. It’s lovely imagery that could be taken right out of a Viagra commercial, we’d never notice the difference, and it’s boring. Meanwhile, a man in a viking helmet crushes a beer can against rock hard abs as he screams a victorious war cry at his latest crypto trade, a woman wearing enormous fake glasses with the complexion and appearance of a supermodel points a manicured nail at a complex-looking candlestick chart, and a dwarf in a polo shirt excitedly scribbles on a whiteboard, all promising guaranteed and immediate financial returns, nay, immediate and guaranteed returns on the quality of your life!

So why the incredible difference in tone between the polo dwarf’s whiteboard and the happy beach couple? Regulation. I hate to say it, but regulation of financial media might be one of the few things the government has gotten more right than wrong, and mind you, I say that begrudgingly. Simply put, history has been replete with con after scam after ponzi after grift, such that for regulated firms and entities, the laws make it impossible for all but the most creative marketing departments to create content with any meaningful pizzaz. Words like “guaranteed” are all but forbidden and claims of outcomes and results are effectively illegal.

For example, in my early career, I placed an ad in a golf course guide (never again) and my original submission to compliance for the language included the phrase: “The only thing you should have to worry about is your short game.” The ad was rejected by compliance with the note: “Should is irrelevant. People have many things to worry about in their finances. Telling them that they shouldn’t worry is misleading.” Apparently even the ideal world hinted at by the word “have” was crossing a hitherto unknown regulatory line. Yet, none of this stops a non-stop deluge of grifters and “educators” from sowing fear, doubt, greed, and misinformation throughout the media space. It is the proverbial “sex” next to the otherwise bland and unappealing mayonnaise sandwich of traditional financial marketing.

What’s so tempting about sex?

Ignoring the obvious literal answer to the question above and thinking about our financial world again, it’s simple: The conventional and traditional financial marketing and media are required to be conservative in their projections and assumptions; to include disclosures and disclaimers. It’s hard not to be tempted by someone posting daily videos of themselves driving Lamborghinis to beaches, surrounded by attractive people, standing in front of audiences giving speeches as they show you the endless green numbers on their trading app of preference. Nevermind that the Lambo is rented, the attractive people are starving actors in LA, and the same actors are in the audience for the staged speech. And the app? Could be true, could be false, but more importantly, whether true or false, it’s not something you can do. And I mean that literally; if you have a functioning time machine, you can crush the markets by the power of hindsight. But no matter what someone shows you on an app or a screen about what they have done, you cannot will that same exact trade or bet into existence in the present. Things simply, have changed.

And of course, deep down, you know this. It’s the same as every time you pick up a book by a Yale professor claiming to be on the fringe of their field of science; despite the fact that they hold tenure at an ivy league university, you are easily tempted into believing that this person might just be the maverick telling you the secrets as to “how it really is.” Even after the secret is revealed and you remember that they’re a tenured professor, you still wonder if you’ve actually been given a taste of some sort of forbidden fruit. The psychology behind being tempted by a financial grifter is no different. Despite the fact that they lack any and all credible credentials, they speak with such confidence and assertiveness that you can easily be led to think that maybe, just maybe, they know what they’re talking about.

Think that you’re immune from such influences? Consider this: Eight influencers were charged with a $114m dollar pump and dump scam at the end of 2022, using nothing but social media to spark interest in their investments. A man with a background as a granite countertop salesman has accumulated over a million tiktok followers and sells so much of a “proprietary” financial product to hapless rubes that he now makes more money selling the marketing funnel for that product to other brokers than he does selling the product itself, despite the fact that the product has been empirically shown not to work as claimed. Even Bernie Madoff didn’t have to put out ads to sell his Ponzi scheme. Merely the unbelievable returns he offered were the “sex” that others whispered to their friends about at the country club and charity galas. “Have you gotten your money in with Bernie? It’s incredible.”

Ending a Pornography Addiction

If you’ve read any of the empirical literature on wealth accumulation in the United States, it essentially indicates that substantial wealth typically arises as the result of one of two paths: Either an incredibly risky bet on entrepreneurship (starting a business, creating a rental empire, becoming a successful artist and celebrity) or a low risk but longer-term bet on consistent saving and investing. While we’ve all heard a dozen stories about how a fry cook became a millionaire by buying Bitcoin when it was seven cents on the dollar, that’s simply one incredibly extreme variation of the first option. So keep that in mind when someone is out there telling you that you can easily become rich “with this simple technique” or “triple your retirement income with a single product.” “There is no free lunch” as the saying goes, and you’d be best to be mindful of that fact. Ultimately, you need to decide what’s more meaningful to you: Living your life and accumulating wealth steadily over time or chasing the next titillation around the corner.

Dr. Daniel M. Yerger is the President of MY Wealth Planners®, a fee-only financial planning firm serving Longmont, CO’s accomplished professionals.

Comments 2

Catchy title there, Dan. Got my attention!

As usual, good advice that I needed years ago. By now I have learned my lesson.

P

Very interesting! Thanks for sharing your insights.