If you’re a regular reader of our blog, you may have noticed that we typically avoid discussing markets too much. This is because, while as investment managers we’re beholden to our duty of care to clients that we must monitor such things, we also keep in mind that overreliance on current events in the markets, the economy, politics, or other considerations often drives investment behaviors that are counter-productive to long-term wealth building. You see, the trick of the matter is that there is always “something” going on, but through the narrow lens of the news we consume, the gossip around the office, or what our hotshot investment guru brother-in-law tells us, we often find ourselves chasing after things that have already happened.

For example, it was only after gold shot up to an all-time high north of $5,000 an ounce that we started having people ask us about it. Not when it was under $2,000 an ounce as recently as late 2023, nor when it was at a relative low of around $1,200 an ounce in the last decade. In what other world than investing do we get excited to pay for something when it has gotten far more expensive than when it was cheap?

One might fairly then try to argue that the stock market is similarly overvalued. “But Dan,” you’d say, “The S&P has never been more expensive!”*

*Pending the recent volatility, but that’s of de minimis concern.

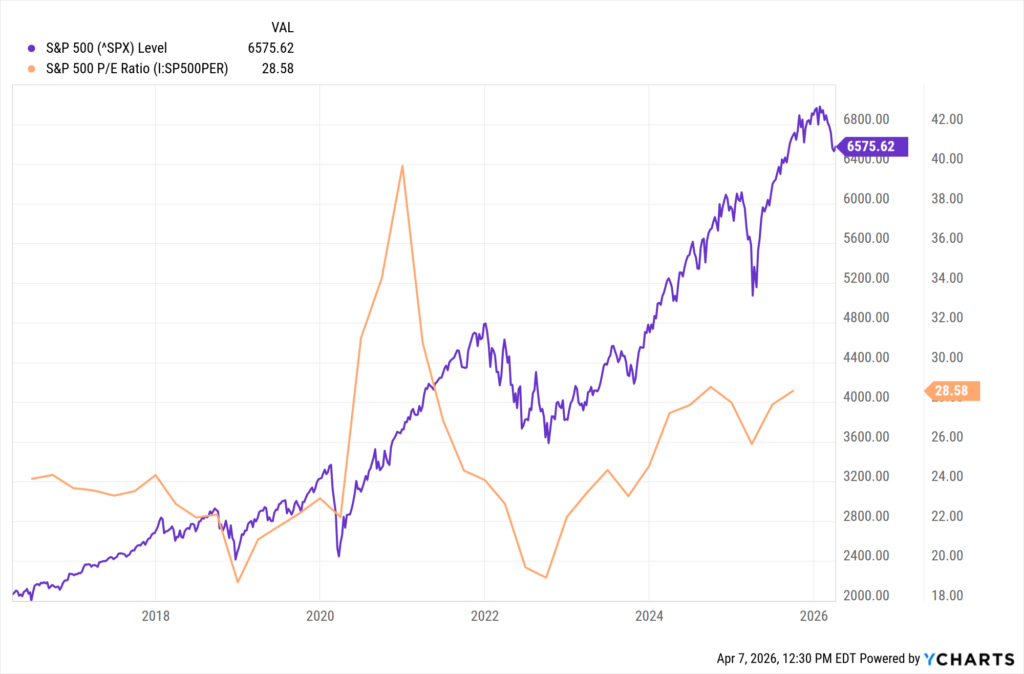

Au contraire, my friendly reader. While the S&P 500 currently sits at 6,575.62 as of this writing, a mere 5.77% off of its all-time high of 6978.60, it’s price-to-equity ratio (“PE Ratio”) sits at 28.58; in other words, you’d have to hold the companies of the S&P 500 for 28.58 years at their current level of profit to pay off the cost of buying them. Sounds expensive, but if we go back a little more than ten years, we’d see that the PE ratio of the same index was 39.9 in the 4th quarter of 2020; the same time that the S&P 500 index was trading at 3,727.04. In other words, the index is not only 28.37% cheaper than it was five years and a quarter ago, but it’s 76.434% more valuable.

You can fairly argue that we’re cherry picking, and here we certainly are. But it hopefully drives home a point that undergirds our investment philosophy: Running around trying to pick up pennies at the risk of being crushed by a steamroller is foolish behavior when you’re far safer simply investing in ownership of the steamroller. So today, we’re discussing the specific elements of our investment philosophy and investment policy, and what undergirds our particular approach.

Our Investment Philosophy & Policy Statement

For those curious to read it in its plain form, here is a copy of our current investment philosophy and policy statement. You may want to set up this blog and the policy statement side by side as we go through it bit by bit.

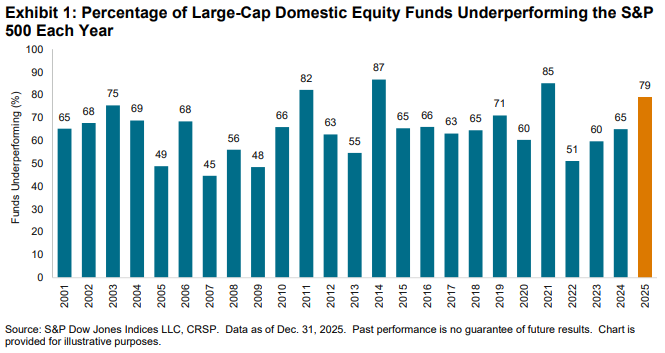

As stated in the document, we emphasize alignment with financial plans and the accomplishment of long-term financial goals and objectives. While being responsive to the crisis du jour is always a topic of conversation among those excited, anxious, or concerned about current events, this is never our driving purpose. Not only because we’re a small firm that cannot begin to compete with larger firms with more robust research teams in the pursuit of finding opportunities to create excess return, but also because almost every year, the majority of such well-funded firms are statistically bad at it despite all their resources and efforts.

(Source: S&P Global)

But because the risk of mistiming far exceeds its potential rewards. Much as we’d all like to have bought any given stock or fund on its lowest day before it shoots to the top of the charts, the probability of that happening even once is staggeringly poor, let alone attempting to do it repeatedly over a period of decades. As I put it in the quote to start Chapter 19 of my new book: “Technical analysis** is astrology for men.” -Anonymous

**Technical analysis is the investment strategy you often see in movies and videos where otherwise “smart” investors are watching the trends and movements of the market through charts and screens and attempting to day-trade their way to success by predicting and timing the movements of the charts and screens. To this day, there is no reliable academic evidence supporting this method of investment.

Why ETFs?

If you’re still reading along with the investment policy statement, then the next stop on the journey is our preference to use exchange-traded funds in client portfolios. While we focus on the use of these products in the document, we don’t discuss very fully “why not alternative options?”

First and foremost, let’s discuss the variety of other investment products. While we do make limited use of cash, mutual funds, money markets, and other types of investment products, we largely avoid the bulk of these where possible because of considerations of cost, liquidity, marketability, or performance. For example, we run relatively low cash portfolios because cash is a poor investment asset. While most brokerages and banks offer some general yield on cash, it seldom keeps pace with inflation; while something like a money market fund or account can better hedge this type of issue, we generally reserve their use for emergency fund balances or near-term expected events where liquidity will be necessary. Otherwise, such cash and cash equivalents simply don’t compare well long-term with equity and bond funds.

With regard to limited use of mutual funds, closed-end funds, or unit investment trusts, we typically look at these as either suffering from tax-efficiency issues or cost issues. While there are tax-efficient versions of all these investment products, many will generate excess ongoing dividends, interest, or capital gains, none of which suit our tax-efficient purpose. And while we could reasonably say that the problem is less of an issue in retirement accounts, we want to default to tax efficiency, not only because of its value in non-retirement accounts but also because research has shown a negative correlation between trading frequency and long-term performance. A nice feature of exchange traded funds compared to many other more active products is that those that track indexes effectively never trade other than when there are new entries or exits from the index.

Finally, with regard to why we don’t get into stock picking (“Why not Nvidia/Apple/Microsoft/Bitcoin/etc?”), we already said it above: There are hundreds of well-funded institutions with billions or even trillions under their management, and statistically, despite their enormous resource advantage, they typically struggle to perform long-term. Thus, we eschew the temptation to pretend we’d do any better with 1/1,000th or fewer resources.

Trading, Rebalancing, and “Should we do something?”

One of the most common questions we’ll get in a meeting with clients who are concerned about the markets is, “Should we be doing something?” or “Should we be making a change?” Much like the sudden interest in gold over the past few months, this question is never asked when the market is shooting up to new all-time highs, only in the context that things are some version of “scary” at the moment, and thus “perhaps we should do something about that.”

The nature of the market and life is that nothing happens in a straight line. Articulated well by our friend Carl Richards, your path from the present to your intended destination will vary over time. When we look at something like “Should we be trading” or “should we be changing investments,” that decision is seldom, if ever, dictated by the current market conditions on a large scale. We are either making a change because of one of the triggering events we describe in our investment policy (drift from original allocation, necessity to raise cash for distribution purposes, etc.) or otherwise are making a change based on our investment research, which is rarely dictated by the volatile nature of the market conditions of the day.

With respect to how we establish what we invest in? Simple: We favor consistency over excellence. While it’s easy with an investment screener to search for the best current return, 1-year, 3-year, or 5-year return, these are less meaningful figures to track because they have already happened. More importantly, we look to compare investment funds and options between like peers, e.g., a large cap blend fund to a large cap blend fund, and then assess across over a dozen metrics how each one compares to its peer group. Ultimately, then, we look for funds that consistently maintain a position in the top quartile when assorted quality and performance factors are aggregated; this means we essentially are never picking the “hot fund” but instead are choosing from a well-curated roster of “old reliables.” From there, we’re assessing that quality on an ongoing basis to evaluate whether that quality persists long term, or if, in the rare case, it doesn’t, work through the process of evaluating alternatives to replace that lagging option.

Investments that Support You Rather than Your Portfolio

Two common issues can arise within the context of how we invest: what about the positions I already have? What about the positions I want or don’t want to have? Let’s discuss each.

When it comes to “legacy positions” already in a portfolio, we’re of two minds:

- Where and when possible to reset a portfolio’s investment allocation to an optimal mix of risk and reward without tax consequences, we should do so.

- Tax consequences can create a mandate that liquidating outdated or less efficient positions be done over a longer period of time to avoid negative tax ramifications or otherwise mitigate them as much as possible.

So what dictates a balance between these two extremes? Simple: What is in any individual client’s best interest? While there is a common philosophy in the financial services industry that “It’s my way or the highway” or otherwise often put down as “Only cash gets in the door,” any individual client’s best interest can be best served by considering the holistic impact of whether a less efficient portfolio is worth weathering for a variety of reasons, whether that be tax efficiency, Medicare premiums, tax credits, or any other variety of balancing tests.

In terms, then, of a client’s demand to include or avoid a particular asset or investment class, we’re always going to ask two more questions:

- If we are demanding the inclusion of a particular investment, what does that investment’s inclusion provide for us in terms of risk and reward that best aligns with your short- or long-term financial goals in consideration?

- If we’re demanding the exclusion of a particular investment, what is driving that desire to exclude? Is it a deeply held moral or ethical belief, a prior life experience, or a concern with investing (or not investing) in a particular asset class for other reasons?

There is no right or wrong answer to either of these questions, but only a clear mandate that we understand your intent in the inclusion or exclusion of such assets and that we build a portfolio that matches both your financial planning needs and your personal intent. While money and building wealth are important, they are a means to an end in living your best life, and mathematical financial optimization should never supersede what that means to you.

Discretion in Our Investment Philosophy

Finally comes the question of discretion, and why we operate with a need to act directly and unilaterally when it comes to client investments. While we’ve iterated our service model substantially over the years, we have come down to a consistent observation, and as a research-based firm, we go where the evidence takes us. While there are plenty of fringe cases and exceptions to this general observation, we have found time and time again that clients’ long-term goals and best interests are best served by having all investments consolidated and managed by one team rather than spread out. Reasons for this can include timeliness of recommendations and changes, tax impacts, portfolio rebalancing timing and efficiency, and even issues of cost or, even more importantly, opportunity costs.

While we have said many times in both the blog and podcast that we can count on one hand a collection of clients who self-manage their investments and do it very well, we’ve found more and more frequently over time that those who insist on doing so are often implementing with varying degrees of timeliness and effectiveness. In the spirit that we always look at money and investments as a means to the end of living a good life, we simply ask this question: If there is no material difference in the cost, but there’s a marked improvement in the results and the effort required to obtain them, what sense does it make to keep your hand on the helm rather than letting someone else steer?

In Conclusion

There is a plethora of valid investment philosophies, policies, and strategies. What works for us may not work for everyone, and whether you’re a fit for how we do things or not is a decision you ultimately get to make for yourself. Ultimately, as fiduciaries to our clients, we desire to serve our clients’ best interests and to assist them in the pursuit of their one great life. With that in mind, we advise on finances and manage investments in a manner we believe most closely aligns with that objective and obligation on our part, and for that, we are privileged to do so. We hope you’ll agree.

Dr. Daniel M. Yerger is the President of MY Wealth Planners®, a fee-only financial planning firm serving Longmont, CO’s accomplished professionals.